From Fur to Autos to Oil, Shipping is Critically Important

From the fur trade to the booming auto industry, shipping infrastructure across the Great Lakes region has been a critical cog in American industry. In his informative and entertaining book The Gales of November, John Bacon reports that 37 of the companies on the Fortune 100 list supported the auto industry and were located in the states surrounding the Great Lakes. A convergence of factors enabled the massive growth of industrial dominance in the Great Lakes region. Raw materials, labor, geographic proximity, and the ability to quickly and reliably transport large quantities of goods created an economic powerhouse. This is similar to the Strait of Hormuz in terms of global oil and commodity transportation. Mr. Bacon tells the story of the S.S. Edmund Fitzgerald, outlining in great detail the limits pushed and the risks taken. These culminated in the ship’s sinking in 1975. In many ways, there was no substitute, given the importance of the cargo and the massive boost in efficiency of moving goods by ship rather than truck or rail.

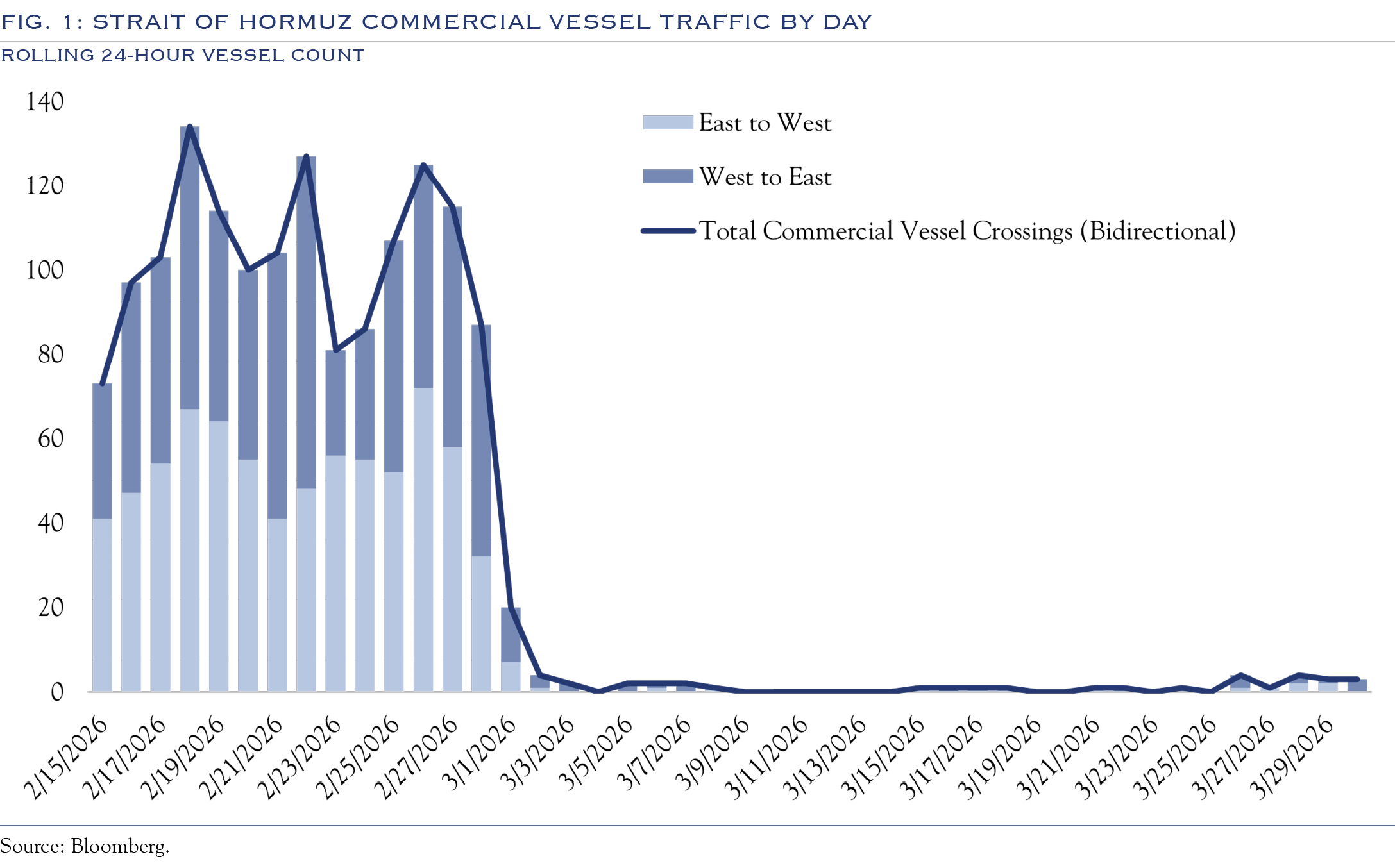

Today, shipping efficiency, the concentration of resources in this region, and the geography of the Strait of Hormuz make it a critical chokepoint for global energy markets. Approximately 20% of the world’s oil flows through this route, highlighting its central role in trade. While alternative routes exist, none fully replace the Strait’s function.

One partial workaround is the Saudi East-West pipeline, which brings oil to the Red Sea and could offset up to one quarter of the stalled capacity. The use of strategic reserves provides another partial (albeit temporary) cushion. Changes in sanctions offer minimal temporary relief. One-off trial transit by vessels making arrangements with Iran is another minimal relief valve. Increased production in the rest of the world is a solution that would require long lead times and would only be initiated if transit is expected to remain closed indefinitely, with sustained high prices to justify new activity.

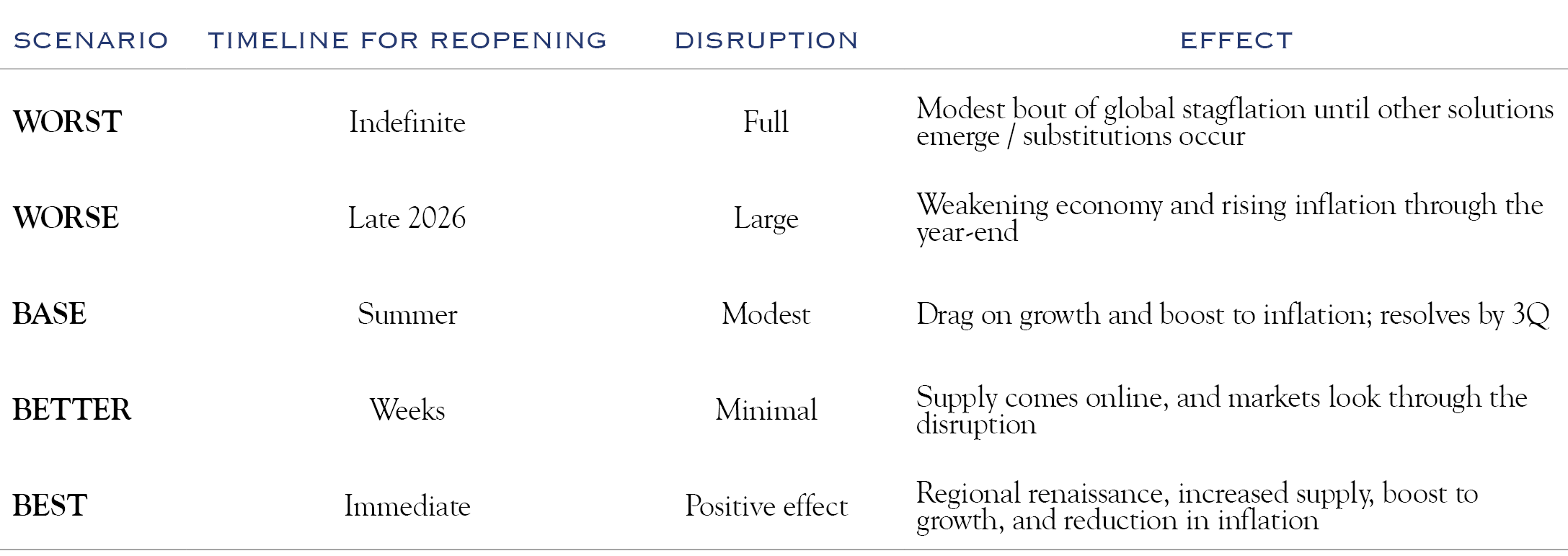

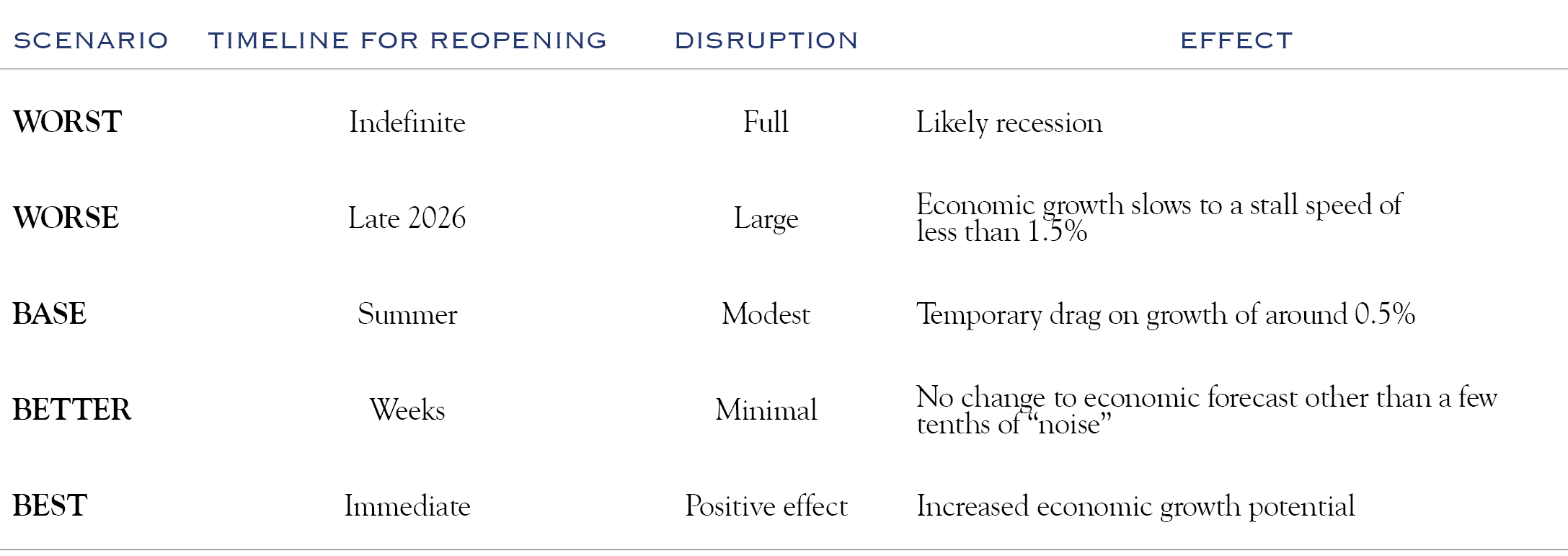

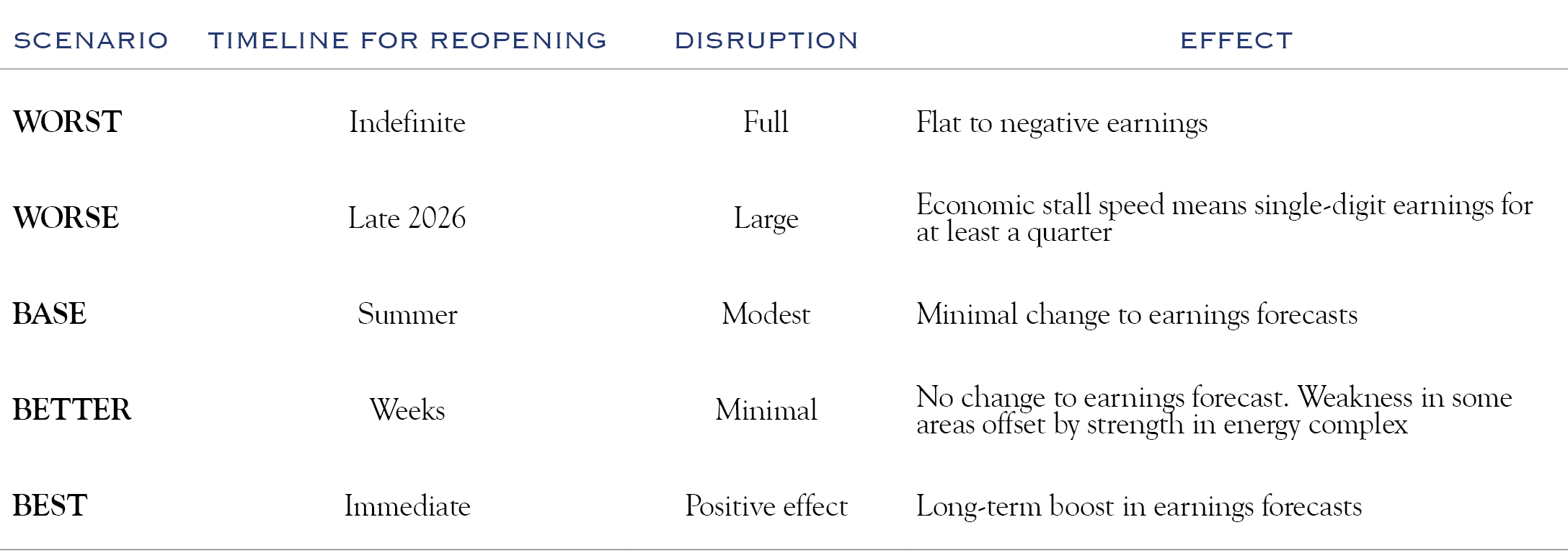

Taken together, this analysis suggests an “endgame” of two possible outcomes. Either the world will continue to face a reduced supply of oil and other commodities, or transit will be mostly restored.

Though the war with Iran has major geopolitical effects, the economic and market impact is clearer. When the volume of oil or other commodities shipped through the Strait declines, prices rise, extending the Fed’s holding period and slowing growth. We therefore map scenarios using key market metrics: cargo ship traffic through the Strait of Hormuz and oil prices.

As a result, while the probability of various outcomes shifts daily, our base case assumes shipping traffic remains disrupted for weeks, but is mostly normal (>50%) by summer.

A partial reopening would not be a geopolitical victory; however, such a development would likely allow markets to turn to other issues as the disruption to oil flows and oil prices becomes clearer and more manageable.

Commercial traffic in the Strait remains low as of March 31, 2026. Increased dialogue between the U.S. and Iran, and support from Gulf States for reopening, raise the chances of a partial or full reopening.

Outcomes range from total permanent closure to immediate reopening, with three stages between.

The range of outcomes will vary globally, and the U.S. will experience less disruption-related pain than many other countries.

Fed Policy

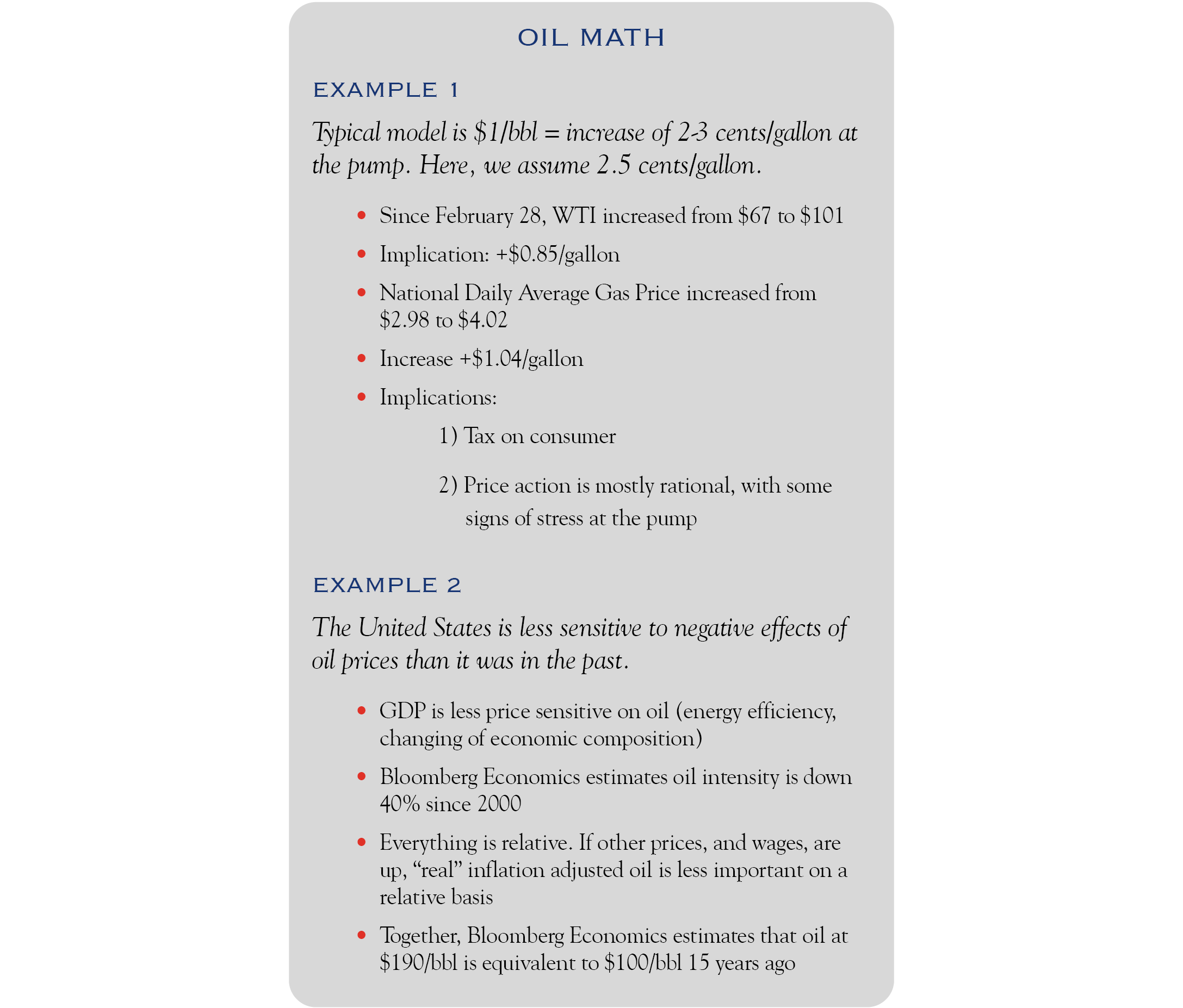

Given the immediate increase in oil prices, the probability of higher inflation has increased. This, in turn, has led to a dramatic change in the outlook for Fed Policy in the near term. So long as the Strait remains closed, the reduced supply of oil and other commodities will lead to upward pressure on inflation metrics. This means the scenario of a “good” rate cut, undertaken with strong employment and easing price pressures, is off the table. Our base case envisions a manageable uptick in pass-through of oil prices, which is not so extreme that the Fed would raise rates. In fact, a rate increase wouldn’t help oil supply and would only reduce domestic demand. Given the current stagnation in labor markets, we think the bar is set very high for a potential rate hike. Far more likely is that rates remain on a “hard pause,” only moving in response to very clear data on either side of the dual mandate. Later in the year, if oil prices normalize, a rate cut could return to the table, especially if the labor market shows any weakness. For now, the situation is simple. Closed Strait = Fed on Hold.

Economy

Expectations for economic growth were rising, fueled by policy stimulus via changes in both individual and corporate taxes. This boost is being offset for consumers by higher gas pump prices and, for both consumers and corporates, by uncertainty over the near-term outlook, given the disruption in the oil market.

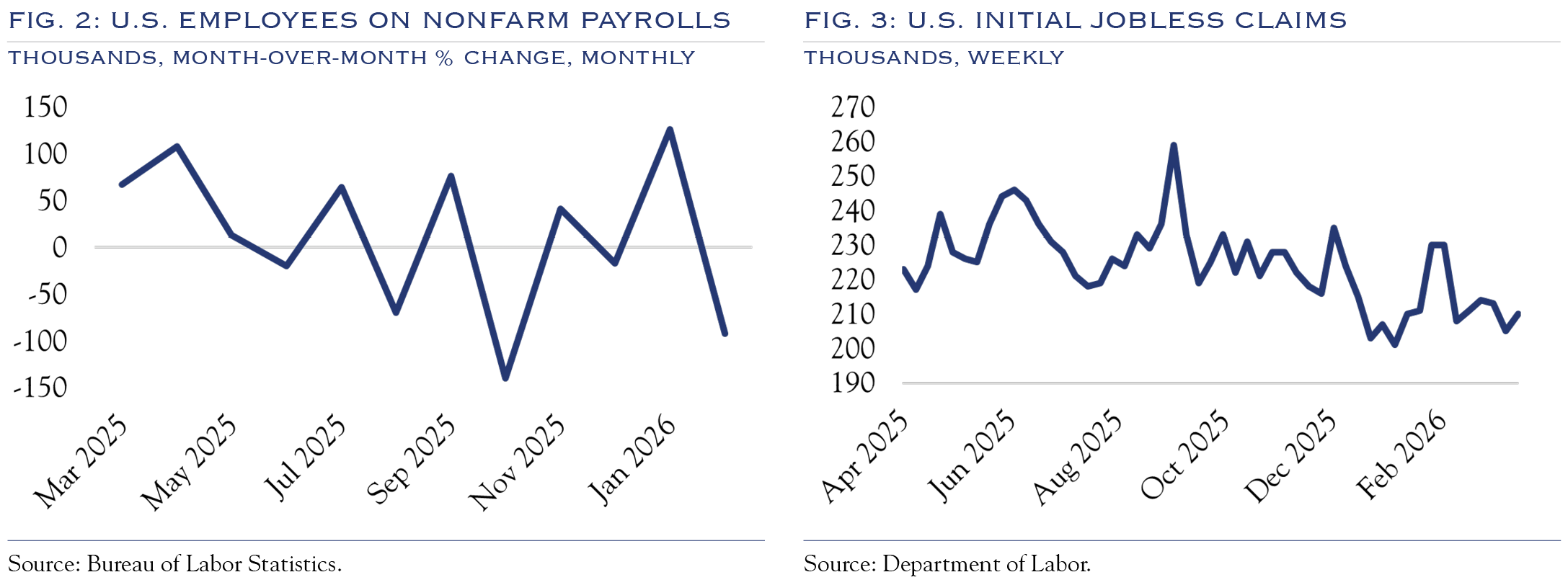

The trend in growth expectations for the U.S. economy is about 2.0%, though it has been sliding amid concerns about the “consumer tax” from higher oil prices. Labor markets have remained stable, with a continuation of the no-hire, no-fire economy. Payroll gains have remained minimally positive over the past year, though the trend is weakening. Weekly jobless claims remain remarkably stable. While both series are influenced somewhat by declines in government payrolls and ongoing healthcare hiring, AI-enhanced productivity is likely also playing a role. More companies are referring to attempts to minimize hiring while using AI to boost efficiency. In other words, no hiring and no firing.

Economic Outlook

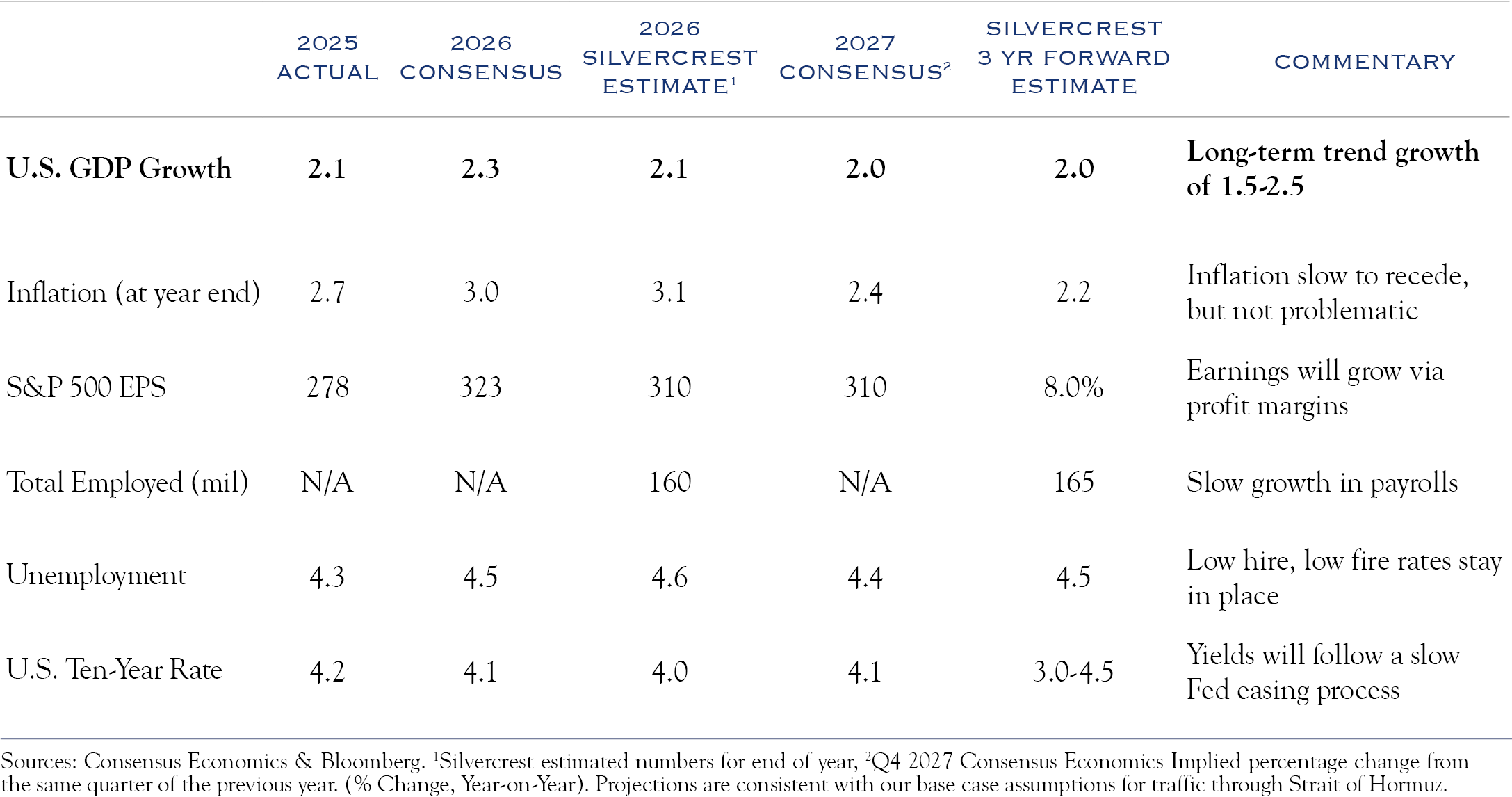

Following our base-case outlook for oil, growth averaging +2.0% to +2.5% is anticipated, but would decline the longer the Strait remains closed. Inflation is likely to tick higher in the near term, though normalization of oil prices by summer would minimize the long-term damage. This will keep the Fed on hold at least until late into the second half of the year. The labor market is expected to remain stagnant.

Earnings

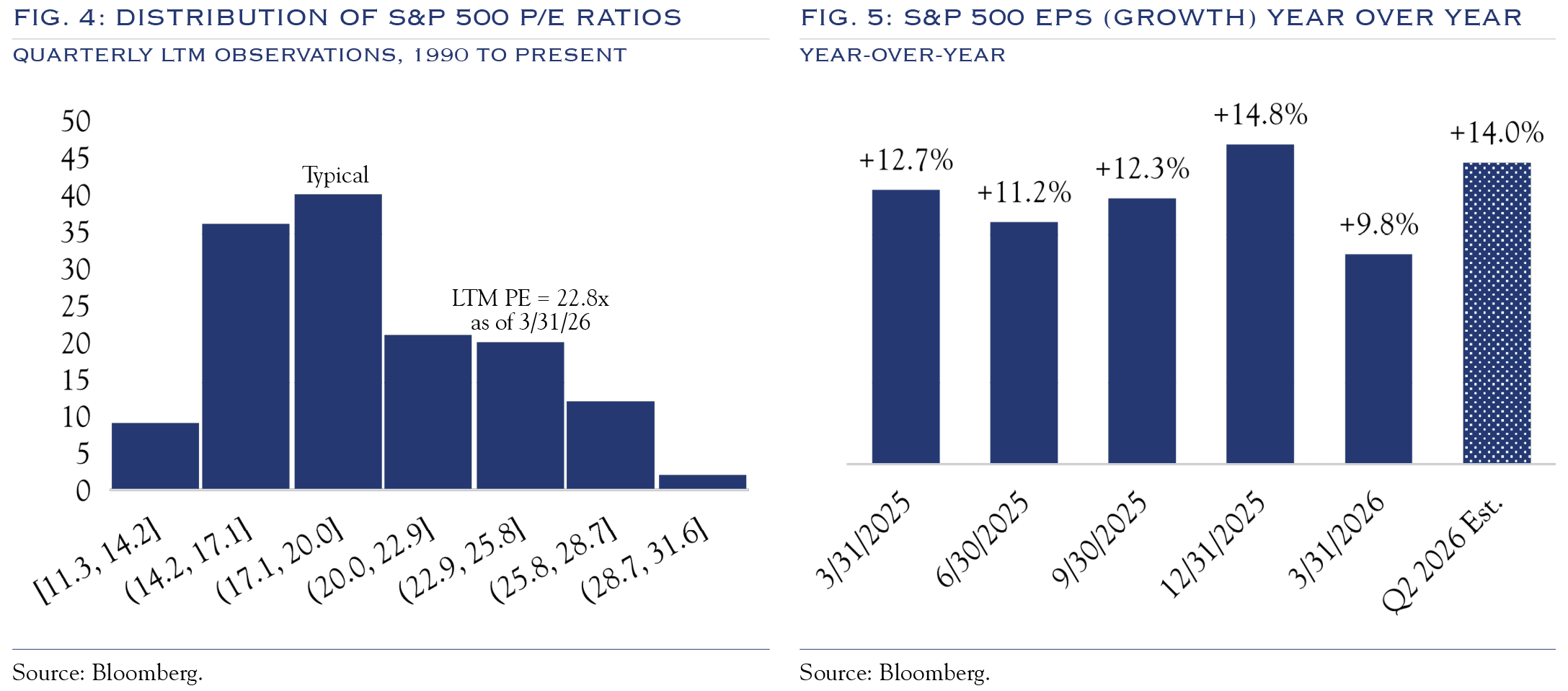

Current consensus forecasts project mid-teens S&P 500 earnings growth this year and next. In previous cycles, analysts underestimated profit margins; however, we caution that current forecasts may be overly optimistic. Many projections assume pronounced economic and productivity gains over the next few years, but without resolution in the Middle East, growth may instead stagnate.

Equity valuations remain elevated, despite modest improvement driven by strong earnings and flat stock prices. Currently, valuations rank in the top 25% vs. the last 35 years.

Despite lofty valuations, strong earnings can fuel stock gains, but recently, stocks have stagnated even with strong results.

This lack of response to strong earnings was a contributing factor in our decision to move to a risk-neutral posture (equal weight equities vs. target). It appears that markets are paying closer attention to a host of issues that have no easy resolution:

- Elevated valuations/high expectations

- Fed policy

- Concerns over private credit

- A lack of clarity about the effect of AI on labor markets

- Emerging risk from the Middle East/Oil

Equity Outlook

In the short term, the path forward depends almost entirely on geopolitical risk, especially the flow of commercial vessels through the Strait of Hormuz. In the intermediate term, focus will likely shift to unresolved issues, keeping valuations in check. If the oil market normalizes soon, the earnings story remains intact. Decent economic growth should power low-teens earnings gains and support equity gains over the long run.

We continue to advocate for balanced positioning between growth and value. Growth stock valuations have improved due to strong earnings. We still expect strong divergence at the company level, as companies must adapt to rapidly changing productivity tools.

Across market caps, we continue to see appeal in small-cap stocks over the intermediate term. Near term, the “flight to safety” trend may limit the appeal of smaller companies, particularly those more sensitive to higher interest rates. However, as the oil and rate backdrop normalize, M&A activity will ramp up, and earnings gains are likely to spread.

Outside the United States, conditions remain volatile, as many markets are more sensitive to oil due to reliance on energy imports. Longer-term, as the world becomes more locally focused, we like the diversification benefits of non-U.S. equities.

Fixed Income

Given the potential for economic stress, we continue to recommend intensive credit analysis. For bond yields, the short-term path will remain highly volatile, with daily activity correlating to the near-term outlook for oil prices. Over the intermediate term, we expect a return to a range-bound 3.75% to 4.25%. In the longer term, yields on the U.S. Ten-Year Note will follow the Fed’s policy lower as the Fed eventually normalizes policy to address stagnant labor markets.

This communication contains the personal opinions, as of the date set forth herein, about the securities, investments and/or economic subjects discussed by Mr. Teeter. No part of Mr. Teeter’s compensation was, is or will be related to any specific views contained in these materials. This communication is intended for information purposes only and does not recommend or solicit the purchase or sale of specific securities or investment services. Readers should not infer or assume that any securities, sectors or markets described were or will be profitable or are appropriate to meet the objectives, situation or needs of a particular individual or family, as the implementation of any financial strategy should only be made after consultation with your attorney, tax advisor and investment advisor. All material presented is compiled from sources believed to be reliable, but accuracy or completeness cannot be guaranteed.

© Silvercrest Asset Management Group LLC