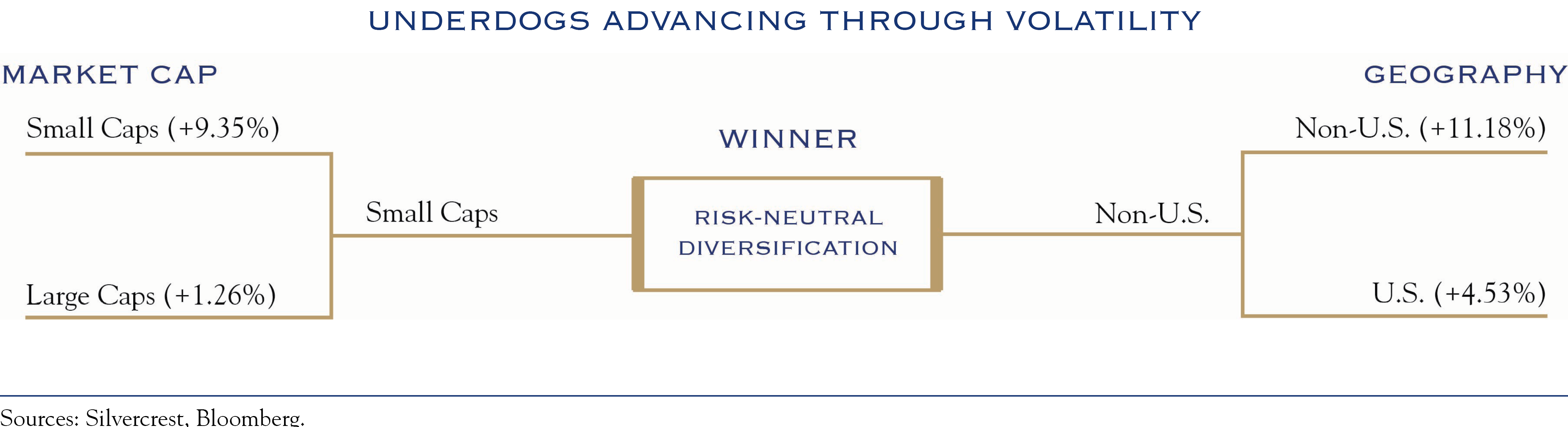

March kicks off a series of celebratory events, like spring training, St. Patrick’s Day, and March Madness that coincide with the changing of seasons. For markets, the current narrative is clearly less festive, with the S&P 500 Index managing a gain of only +0.49% in 2026. This gloom derives from economic uncertainty, AI anxiety, and financing fears. While each concern presents a legitimate risk to the long-running bull market, we still see a positive though increasingly turbulent backdrop. This isn’t unusual, particularly when a leadership change is unfolding. Indeed, underdog small caps have led the way with a return of +6.10% vs. +0.65% for large-cap equities.

Across the 40-year history of the 64-team NCAA basketball tournament, underdog success stories are a joy to behold. In the women’s bracket, major upsets have been rare, with only one instance of the lowest-seeded team (#16) defeating the top-ranked team (#1), and no instances of #15 defeating #2 or #14 defeating #3. The men’s tournament has seen a few more examples of underdog success: two instances of the lowest-seeded team (#16) defeating the highest-seeded team (#1), 11 instances of #15 defeating #2, and 23 games where #14 defeated #3.

A personal favorite is the 2005 victory by the Bucknell Bison over the Kansas Jayhawks on a last-second shot.

Since a broader set of winners is a key support for an extended bull market, we hope the stock market follows the pattern of the men’s tournament. Thus far in 2026, it has, as the underdogs have emerged with non-U.S. stocks, small-cap companies, and sectors such as Energy, Materials, and Industrials leading the way.

Leadership in those areas often foreshadows increases in economic activity and earnings. As a rule of thumb, markets tend to lead the economy by four to six months. Small caps and cyclicals at the front of the pack could be an early sign that economic activity is poised to accelerate. A recent newsletter by Macro Man Cameron Crise on Bloomberg finds that the highest correlation between stock prices and earnings expectations occurs seven to ten weeks out. Both insights support the view that markets are anticipating an increase in economic activity and earnings. Thus far in 2026, however, only minimal upward movement has emerged in expectations for GDP or earnings. The clock is now ticking for clear evidence of an improving economic and earnings cycle.

Overall, we see this as the end of the beginning for the bull market, with powerful themes transitioning to more mature and complex phases. This means a less ebullient and more volatile environment. Progress will come in fits and starts rather than a simple, accelerating upward trend.

Pillar 1: The Economy—Stable and slowing

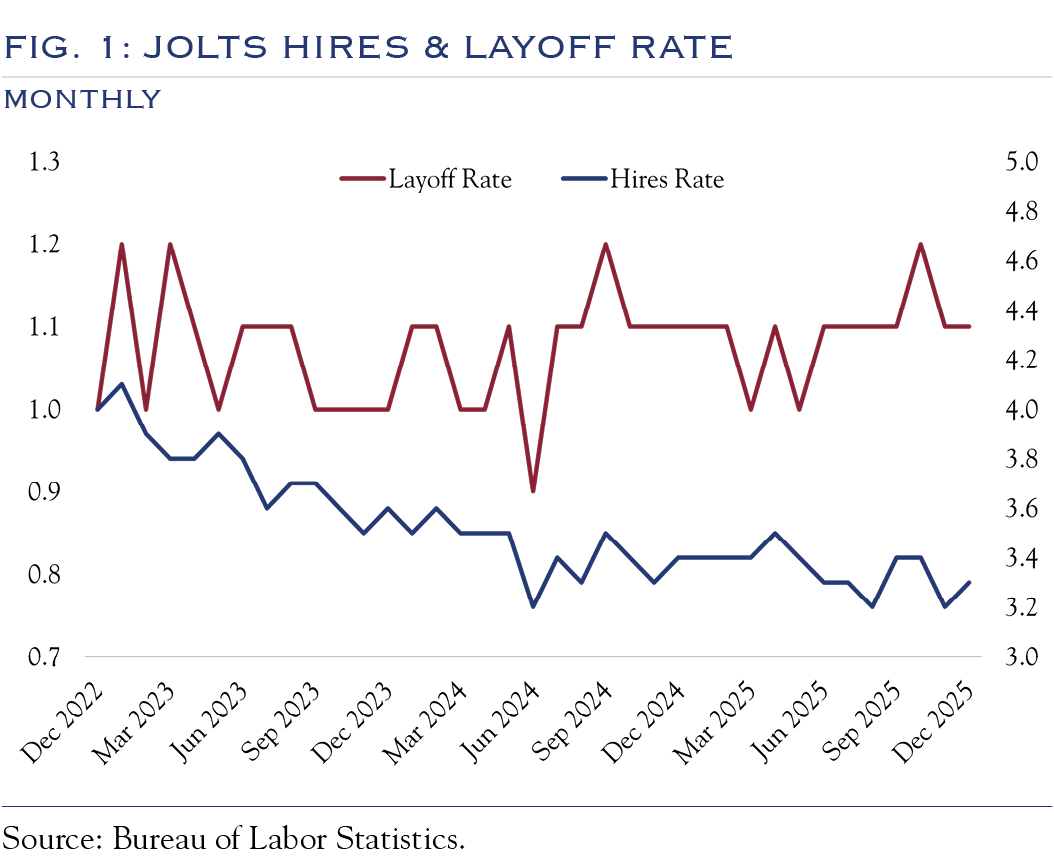

Modest payroll growth and limited layoffs indicate that labor market conditions remain stable but sluggish.

Jobless claims, payroll changes, JOLTS metrics, and private market data all paint a similar, mixed picture of the labor market.

Consumer spending data is similarly mixed, with the upper part of the K-shaped recovery continuing to be fueled by wealth-effect spending, while lower-income consumers struggle with the aftermath of inflationary price pressures.

Businesses are once again reminded of the uncertain backdrop, with recent changes in tariff policy and ongoing geopolitical stress highlighting the instability.

Our real-time metrics point to growth hovering around +2.0 to +2.5%. So long as growth remains above +1.5%—and we believe it will—the backdrop remains conducive for solid earnings growth.

Pillar 2: Private Financing Backdrop

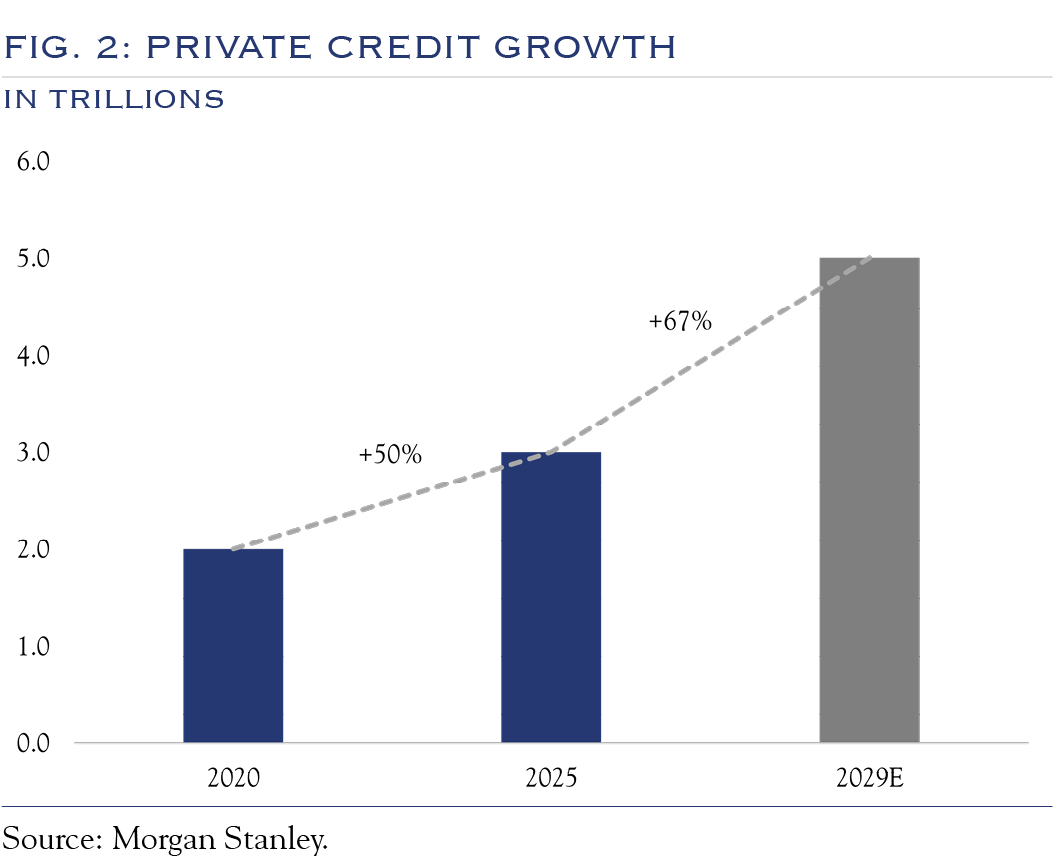

The interest rate picture is evolving slowly, and credit spreads remain very favorable. The biggest change in the financing environment has been the rapid growth of private financing in all its forms. See Figure 2. Given recent concerns over liquidity mismatches, the flywheel may begin to slow. We anticipate slower growth in private financing, not a wholesale reversal. At the margin, this restricts the expansion of financing and likely puts a small drag on potential growth. In the current environment, close monitoring of liquidity terms and credit risk is essential.

Pillar 3: The AI Theme

A growing number of examples point to the effectiveness of AI. Some recent reports suggest that this effectiveness is sowing the seeds of its demise, with AI displacing enough workers to cause a recession. We see two missing components in that argument. First, the timeline for AI’s capabilities is not the same as the timeline for its adoption by corporations, employees, and individuals. Just because something can be done more efficiently doesn’t mean it will be done that way immediately. We expect timelines to diverge, with vast differences emerging between those who adapt and those who don’t—setting the stage for a renewed opportunity in active equity management. Second, the more apocalyptic analyses ignore follow-on effects. The increased profits have to flow somewhere. Creative destruction in the economy may cause anxiety, but it has been proven to spur economic growth.

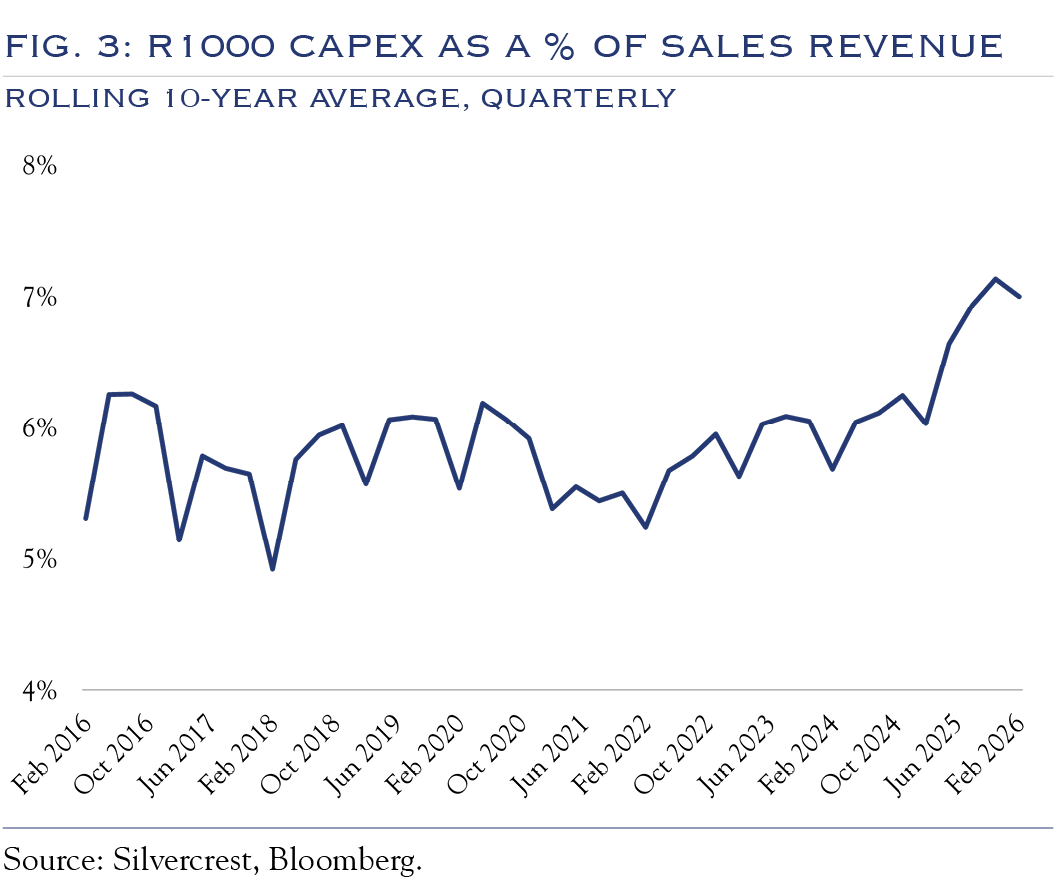

AI has been a critical driver of equity market returns and economic growth. We see the continued build-out of AI-related capital expenditures as supportive of GDP expansion. For example, UBER’s capital expenditure became a de facto subsidy for riders; similarly, the AI spending underway should ultimately benefit users through increased competition and declining costs. Despite the turmoil caused by projections of winning and losing industries, we anticipate continued productivity gains and opportunities for profit margin expansion across a broad swath of the equity market. Meanwhile, some challenges may continue for areas where significant enthusiasm is already embedded in prices/valuations and where competition has increased.

As AI continues to evolve, competition will increase, costs will come down, usage will increase, and the long-term benefits will accrue to the most intelligent users of the technology.

Outlook

The economy, private financing, and the AI theme all show signs of slowing—but not reversing. For now, the rotation appears to be driven by rebalancing, risk mitigation, and an expectation of accelerating economic growth and earnings. So long as the three pillars remain stable rather than deteriorate, we expect volatility and rotation to continue, which will eventually lead to a broader, healthier equity market advance with modest gains powered by earnings. Should further weakness materialize in either the economy, private financing, or AI, valuation compression would outweigh earnings, and stocks would struggle. The market backdrop has become more complex. In this environment, we recommend a simple portfolio configuration—risk-neutral, with a healthy dose of diversification into smaller companies and non-U.S. equities.

This communication contains the personal opinions, as of the date set forth herein, about the securities, investments and/or economic subjects discussed by Mr. Teeter. No part of Mr. Teeter’s compensation was, is or will be related to any specific views contained in these materials. This communication is intended for information purposes only and does not recommend or solicit the purchase or sale of specific securities or investment services. Readers should not infer or assume that any securities, sectors or markets described were or will be profitable or are appropriate to meet the objectives, situation or needs of a particular individual or family, as the implementation of any financial strategy should only be made after consultation with your attorney, tax advisor and investment advisor. All material presented is compiled from sources believed to be reliable, but accuracy or completeness cannot be guaranteed. © Silvercrest Asset Management Group LLC