In this issue of Insights, our team explores some of the most consequential forces shaping today’s markets and economy: the structure of the AI buildout, the philosophy of portfolio construction, and the geopolitical shifts reshaping how capital is deployed around the world.

Introduction

Richard R. Hough III

Chairman and CEOIn this issue of Insights, our team explores some of the most consequential forces shaping today’s markets and economy: the structure of the AI buildout, the philosophy of portfolio construction, and the geopolitical shifts reshaping how capital is deployed around the world.

Brian Bies, who manages our U.S. Small Cap Growth and SMID Growth strategies, writes “Edge AI: The On-Device Frontier Beyond the Data Center.” Brian draws a contrast between the massive centralized data centers commanding investor attention today and the next wave of AI: smaller, untethered, and embedded. From robotics to wearables to space, he argues that distributed intelligence is still in early stages and is already demanding new architectures.

In “Efficient Diversification: The Case for Fewer Holdings in Active Portfolios,” Chris Richey, a portfolio manager on our Focused Value team, challenges the assumption that more holdings means better risk management. Drawing on decades of academic research, he makes the case that returning to the optimal range requires something too rarely practiced in our field: restraint.

Senior analyst Marcus Viscichini presents “How Fund Structure Shapes Outcomes: A Practical Guide.” He reminds us that choosing the right investment vehicle is often as consequential as choosing the strategy itself, walking through tax efficiency, liquidity, fees, and jurisdiction across both public and private markets.

In “Sovereignty Over Efficiency: The Return of Industrial Policy,” Kevin Hill, another portfolio manager on our Focused Value team, explains why the efficiency-first framework of the past several decades is giving way to one centered on resilience and domestic capacity. He traces the historical roots of this shift and considers what it means for portfolios today.

Thank you for reading this edition of Insights. We are grateful for the opportunity to share our thinking with you.

Economic & Market Overview

- The economy remains on solid footing, though the pace of expansion has cooled. Policy stimulus from tax changes and deregulation is now partly offset by higher oil-related costs and geopolitical uncertainty.

- Labor market data remain mixed but broadly stable. The hires rate has held in a narrow band around 3.2% to 3.4%, consistent with a “no-hire, no-fire” economy in which layoffs stay contained even as AI-enhanced productivity restrains headcount growth.

- Inflation has reaccelerated even as wage growth has eased, squeezing real incomes and tempering the consumer’s contribution to growth—a shift from the tailwind of the prior year.

- Overall, the expansion continues but with less momentum. The backdrop should remain adequate to support earnings, though in a more volatile, fits-and-starts fashion.

- Our model combines the hires rate, the change in average hourly earnings, and inflation to estimate consumer spending potential. With wage growth easing to about 3.4% as CPI climbed to 4.2%, real wages have turned downward, a marked reversal from the roughly four-point advantage consumers enjoyed a year ago.

- Given the standoff between stagnant labor markets and stubborn inflation, the Fed is likely to remain on a hard pause for an extended period. The 10-Year yield to hold broadly in a 3.5% to 4.5% range—below the danger zone for equities, but not yet supportive of higher valuations.

- Headline CPI has reaccelerated to 4.2% year-over-year as of May, up from 3.8% in April and 2.7% at the end of 2025. The renewed pressure is largely an energy story tied to disruption in the Strait of Hormuz, rather than a broad-based reacceleration.

- Shelter, which carries roughly a third of the index weight, has continued to ease rather than drive the move. Its contribution to headline CPI has slipped to about 1.2 percentage points—down from roughly 1.4 a year earlier—as the Rent and Owners’ Equivalent Rent components gradually normalize, making shelter a secondary driver of the more recent inflation.

- In the near term, the principal constraint on further equity appreciation is valuation. The S&P 500’s forward 12-month P/E ended 2025 around 22x. That was among the highest readings on record, meaning a great deal of good news is already embedded in prices, leaving limited room for disappointment.

- While valuations are a constraining factor, earnings remain the engine. S&P 500 earnings grew roughly 22% year-over-year in the first quarter of 2026, accelerating from about 15% in the prior quarter, with operating margins expanding from around 15% to nearly 17%. The key question is whether those gains broaden beyond a narrow set of AI-related winners.

- WTI has retraced most of the spike, easing to $81.42 (6/15/26) – now only $14.42 (about 22%) above the $67 February baseline, versus the $101 peak seen at the end of March.

- On the rule of thumb, that smaller $14.42 crude move should translate to just $0.29 to $0.43 per gallon of pump-price increase ($0.36 at the midpoint), implying gas prices should have fallen meaningfully as crude came back down. Yet pump prices have not followed crude lower: AAA’s national average is $4.07, actually a touch higher than the March reading and up about $1.09 from the February starting point.

- The direct crude oil supply shock is unwinding, but sticky pump prices keep upward pressure on headline CPI for now. A more favorable setup for eventual Fed easing than in March, though the relief at the pump that lower crude would normally bring has yet to materialize.

Brian Bies, CFA

Managing Director, Portfolio ManagerEdge AI: The On-Device Frontier Beyond the Data Center

While much of today’s AI investment is focused on centralized data centers and cloud infrastructure, Edge AI pushes intelligence outward onto dynamic endpoint devices operating at the edge of the network. The full potential of AI investment will only be realized when that centralized intelligence works in concert with highly capable Edge AI systems.

read the insight

Christopher K. Richey, CFA

Managing Director, Portfolio ManagerEfficient Diversification: The Case for Fewer Holdings in Active Portfolios

Efficient diversification is not a new idea. The evidence has been clear for decades. But committing to it requires all of us in active management to foster a trait that too few in our industry have embraced: restraint.

read the insight

Marcus Viscichini

Senior AnalystHow Fund Structure Shapes Outcomes: A Practical Guide

Investors today have access to a wide range of investment structures, each with meaningful differences in how they are managed, taxed, priced, and accessed. Choosing the right vehicle is often as consequential as choosing the investment strategy itself.

read the insight

Kevin Hill, CFA

Portfolio ManagerSovereignty Over Efficiency: The Return of Industrial Policy

Markets remain effective at allocating resources in predictable systems. But when predictability cannot be assumed, additional constraints come into play. Production capacity, supply chain control, and the ability to operate under disruption become more important.

read the insightInvestment Outlook Summary

From the Investment Policy & Strategy Group

Equities

Continued gains in equities are expected, driven primarily by earnings growth, which will be powered by profit margin expansion. Over the past several years, corporate America has been especially dynamic in adapting to massive change. This dynamism, along with advances in technology, should drive higher profits, with stocks following suit. However, given the elevated state of valuation, risk and reward have become more balanced, and we recommend a posture that is near target ranges for exposure.

Growth & Value

We continue to advocate for a balanced approach between growth and value. The degree to which individual companies can adapt to a rapidly changing environment is more likely to determine success than their designation within benchmark indices. The economy should remain on solid ground, neither accelerating nor falling into recession, so a balance between cyclical and less cyclical components is warranted. Additionally, the degree of exposure to the AI theme has emerged as a new and powerful factor that cuts across value and growth.

Small Cap & Large Cap

Large-cap companies will continue to benefit from their scale, including access to capital markets, the ability to invest in new technologies, and the recipients of index flows. We have maintained and will continue to maintain an outsized allocation to smaller companies. As noted above, the valuation gap, diversification benefit, opportunity for profit expansion as the AI wave unfolds, M&A environment, and tailwinds from eventual rate cuts present a compelling mix.

U.S. & Non-U.S.

We maintain our diversified posture across geographies. Valuation and growth opportunities exist across a broad range of industries, regions, and countries, and we rely on active management to identify these opportunities. Currency should be largely neutral, with a stable to slightly declining U.S. dollar, although the U.S. has an edge over most developed markets due to better demographics and expected growth. Pockets of emerging markets also offer solid growth prospects.

Fixed Income

Credit

We emphasize extreme selectivity with credit risk. Security selection is paramount, with active management as a critical component of avoiding potential problems. We favor more liquidity and higher quality within the credit space. A recent Bloomberg story highlighted the range of prices used by various market participants for the same loan. Given the massive growth in private funding markets against a mostly benign backdrop and with interest rates remaining stubbornly high, it is no surprise that some situations have gone haywire. Our work has consistently emphasized the importance of diligent credit underwriting and security selection, rather than generic and broad exposure.

Rates

Interest rates for the U.S. 10-Year Note will generally follow the path of Fed policy for the foreseeable future. This means that rates will decline, but slowly. Fed policy is constrained by stubborn inflation and a steady but weakening job market. So long as inflation and employment remain mostly stable, rate pressure will ease slowly.

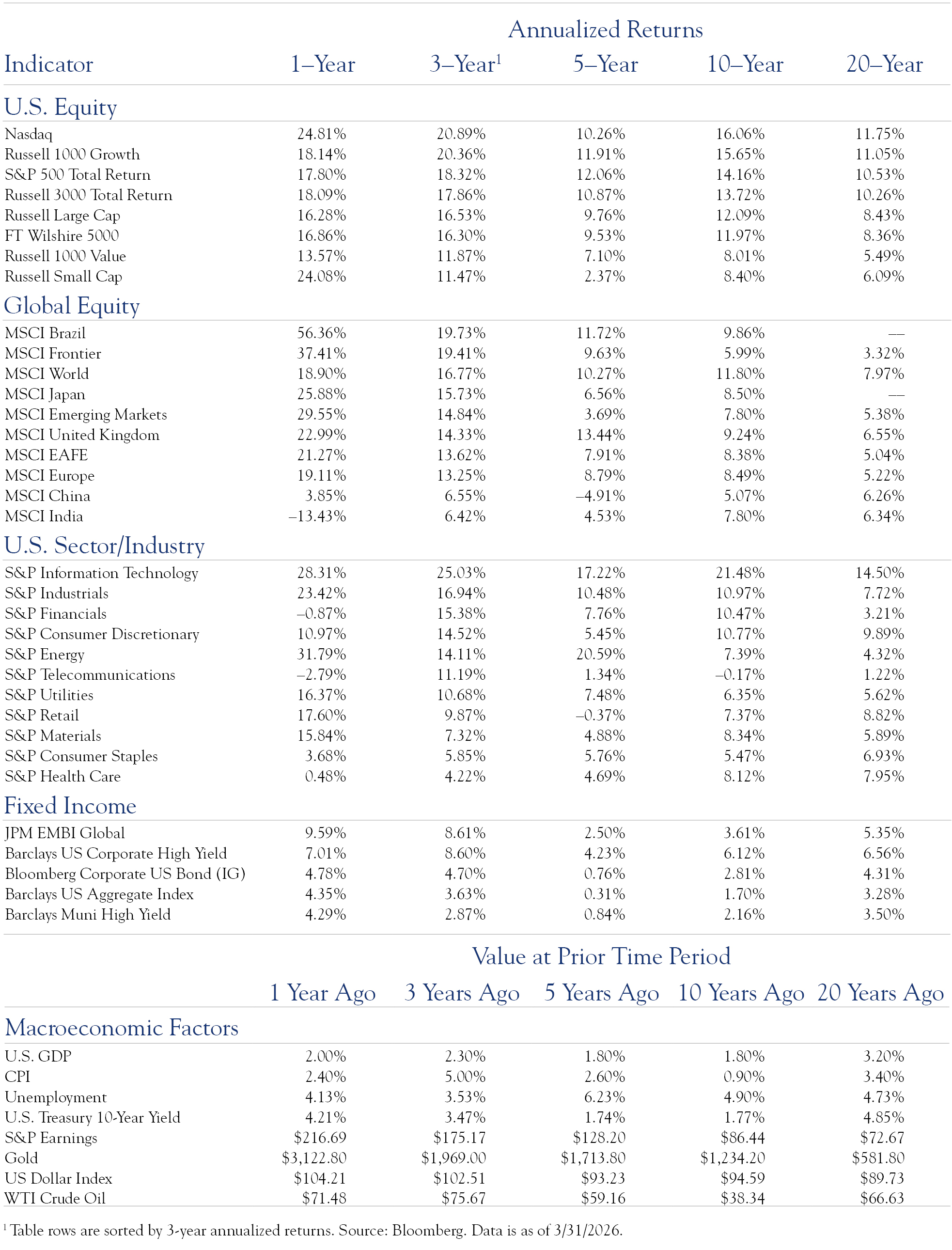

Market Monitor

This table provides a comprehensive view of returns across various markets across time. It is paired with a snapshot of economic data, allowing a comparison of annualized returns while referencing the coincident economic conditions.

This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Before making an investment decision, investors need to consider, with or without the assistance of an investment advisor, whether the investments and strategies described or provided by Silvercrest, are appropriate, in light of their particular investment needs, objectives and financial circumstances. Furthermore, this document is for information/discussion purposes only and does not and is not intended to constitute an offer, recommendation or solicitation to conclude a transaction or the basis for any contract to purchase or sell any security, or other instrument, or for Silvercrest to enter into or arrange any type of transaction as a consequence of any information contained herein and should not be treated as giving investment advice.

This communication was not intended or written to be used, and cannot be relied upon, by any taxpayer for the purposes of avoiding any U.S. federal tax penalties. The recipient of this communication should seek advice from an independent tax advisor regarding any tax matters addressed herein based on its particular circumstances. Investments with Silvercrest are not guaranteed. Although information in this document has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness, and it should not be relied upon as such. All opinions and estimates herein, including forecast returns, reflect our judgment on the date of this report, are subject to change without notice and involve a number of assumptions which may not prove valid.Investments are subject to various risks, including market fluctuations, regulatory changes, counterparty risk, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you may not recover the amount originally invested at any point in time. Furthermore, substantial fluctuations of the value of the investment are possible even over short periods of time. Further, investment in international markets can be affected by a host of factors, including political or social conditions, diplomatic relations, limitations or removal of funds or assets or imposition of (or change in) exchange control or tax regulations in such markets. Additionally, investments denominated in an alternative currency will be subject to currency risk, changes in exchange rates which may have an adverse effect on the value, price or income of the investment. This document does not identify all the risks (direct and indirect) or other considerations which might be material to you when entering into a transaction. For certain investments, the terms will be exclusively subject to the detailed provisions, including risk considerations, contained in the Offering Documents. Review carefully before investing.

This publication contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models and hypothetical performance analysis. The forward-looking statements expressed constitute the author’s judgment as of the date of this material. Forward looking statements involve significant elements of subjective judgments and analyses and changes thereto and/or consideration of different or additional factors could have a material impact on the results indicated. Therefore, actual results may vary, perhaps materially, from the results contained herein. No representation or warranty is made by Silvercrest as to the reasonableness or completeness of such forward looking statements or to any other financial information contained herein. We assume no responsibility to advise the recipients of this document with regard to changes in our views.

This communication contains the personal opinions, as of the date set forth herein, about the securities, investments and/or economic subjects discussed by the Investment Policy & Strategy Group. No part of the members of the Investment Policy & Strategy Group’s compensation was, is or will be related to any specific views contained in these materials. This communication is intended for information purposes only and does not recommend or solicit the purchase or sale of specific securities or investment services. Readers should not infer or assume that any securities, sectors or markets described were or will be profitable or are appropriate to meet the objectives, situation or needs of a particular individual or family, as the implementation of any financial strategy should only be made after consultation with your attorney, tax advisor and investment advisor. All material presented is compiled from sources believed to be reliable, but accuracy or completeness cannot be guaranteed.

© Silvercrest Asset Management Group LLC